Key Takeaways

- Fund administration minimums run $50K-$150K/year regardless of fund size. LP requirements, not AUM, are the real reason to add one

- Software is cheaper than fund admin at every AUM level shown, including $300M; the cost gap never closes

- Outsourced admin gets cheaper as a percentage of AUM as you scale, but still costs 2-3x more than a full-stack software platform at $300M

- Annual audits and complex tax filings require a third party under either model

At some point in every fund’s growth, someone in the room tells you that you need a fund administrator. Your attorney during fund formation. An institutional LP on a diligence call. A peer who made the leap a fund ago. The advice sounds professional, responsible, and hard to argue with.

Then the quote comes back. Seventy-five thousand dollars a year, minimum, before the audit. That number shifts the question from whether to do it to whether you actually have to.

For most GPs, the honest answer is: not yet, and maybe not ever. Software handles the same operational work (distributions, capital calls, investor reporting, waterfall calculations) at a fraction of the cost, at any AUM level. The cost gap never closes. What changes the equation is who your LPs are, not how big your fund gets.

Here is the full cost breakdown and the one factor that actually decides it.

What a fund administrator does (and costs)

A third-party fund administrator handles bookkeeping, financial statements, capital call processing, distributions, investor reporting, and K-1 preparation. Their core value is independence: an external firm’s sign-off carries credibility with institutional LPs conducting operational due diligence.

Three cost components typically combine:

| Cost component | Typical range | Notes |

|---|---|---|

| Annual administration fee | 5-15 bps of committed capital | Percentage applies above the minimum |

| Annual minimum fee | $50,000-$150,000 | Applies regardless of fund size |

| Setup / onboarding | $5,000-$25,000 | One-time; varies by structure complexity |

| Annual audit | $15,000-$40,000+ | Separate from admin; passed through to fund |

| K-1 preparation | Included or quoted separately | Depends on provider and investor count |

Sources: VC Beast (2026), Origin Investments (2024), Anchin (2025)

At $30M AUM, a $75,000 minimum equals 25 bps of committed capital. At $300M, the same minimum is 2.5 bps. Fund administration gets proportionally cheaper as AUM grows, but never cheaper than software.

What software actually covers

Modern platforms handle most of what fund administrators do operationally. What they don’t cover: annual audits and multi-jurisdiction tax filings. Both still require a licensed CPA or legal counsel regardless of which model you use.

| Function | Fund administrator | Software platform |

|---|---|---|

| Bookkeeping and general ledger | Included | Varies; Agora includes accounting services |

| Capital call management | Included | Automated |

| Distribution waterfall calculations | Included | Automated |

| Investor portal and reporting | Usually included | Automated |

| K-1 preparation and delivery | Included | Varies; Agora includes CPA-prepared K-1s |

| Annual audit | Typically quoted separately | Not included; requires third-party CPA |

| Multi-jurisdiction tax filings | Included | Requires third-party CPA |

| ACH / NACHA payment processing | Depends on provider | Included in full-stack platforms |

Based on standard service scopes; verify specific inclusions with each provider before committing.

The real cost comparison

The chart uses fund admin fees at 10 bps with a $75,000 minimum plus a $25,000 audit. Software uses published pricing midpoints.

The non-obvious read: Software is cheaper at every AUM level shown, including $300M. The cost argument for fund administration never closes. What shifts at higher AUM is LP requirements, not the cost math. Pension funds and endowments increasingly require third-party sign-off as a condition of investment. That requirement is what drives the decision at scale.

The AUM inflection point

The real variable is your LP base, not AUM. This framework maps cost against the LP requirement threshold:

| AUM level | Est. fund admin cost / yr | Est. software cost / yr | When to consider fund admin |

|---|---|---|---|

| Under $25M | $75,000-$100,000 | $3,600-$24,000 | Rarely; cost gap is too wide to justify |

| $25M-$100M | $75,000-$125,000 | $12,000-$60,000 | Only if a specific LP requires it |

| $100M-$250M | $125,000-$270,000 | $36,000-$120,000 | If institutional LPs mandate third-party oversight |

| $250M+ | $270,000+ | $90,000+ | Often required by pension funds and endowments |

Cost ranges derived from VC Beast (2026), Origin Investments (2024), Anchin (2025). Software ranges are representative; exact pricing varies by platform, AUM tier, and feature scope.

The LP requirement threshold rarely applies until a fund is actively targeting pension funds or endowments. Until then, software plus an independent CPA for annual audits covers the same operational ground for less.

One structural note worth knowing: fund admin fees are charged as a fund expense, meaning LPs absorb them before returns are calculated. Software licenses are a management company expense paid from the GP’s management fee, which can make software more expensive for the GP personally at smaller fund sizes.

What Agora covers at the software tier

Agora consolidates capital calls, distribution waterfall calculations, investor reporting, document management, ACH and international payments, and a white-labeled investor portal in one platform. Unlike most software, Agora also includes accounting services with dedicated CPAs, covering bookkeeping and K-1 preparation that most platforms exclude. The platform supports 500+ firms managing $150B+ in combined AUM, including institutional-scale opportunity funds.

Annual audits and multi-state tax filings still require an independent CPA firm. Combined with the platform subscription, total annual cost remains well below fund administration minimums, unless LP requirements specifically mandate third-party oversight.

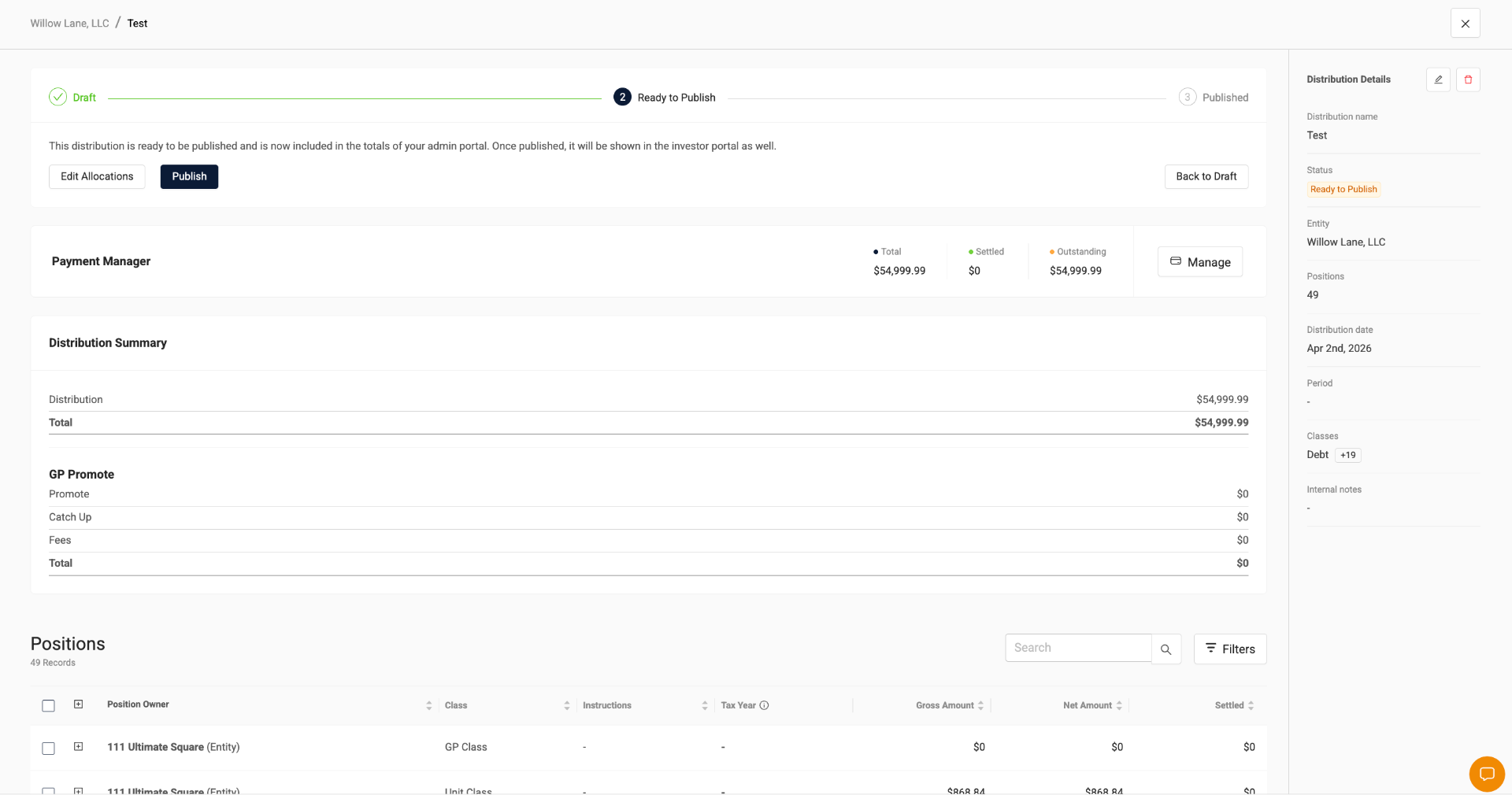

Distributions are where the fund admin vs. software question gets most concrete. A single distribution cycle (waterfall calculation, payment initiation, investor notification) is exactly what fund administrators typically own. In Agora, the GP owns it directly.

Navigate to Investments → Entities → [Entity] → Transactions → Distributions → [Distribution]

The three-stage workflow (Draft, Ready to Publish, Published) keeps the GP in control of every distribution before anything reaches investors. Payment Manager totals, Distribution Summary, and GP Promote calculations are visible on the same screen as the per-position table. Nothing goes out until the GP advances the status. That is the same oversight a fund administrator provides, without the $75,000 minimum.

For most GPs, the decision comes down to one question: what does your LP base require? Cost consistently points toward software. Your investors determine whether fund administration needs to sit on top of it.

See how Agora handles the full fund administration workflow, from capital calls to K-1 delivery, without a third-party administrator.

References

- VC Beast. (2026). 5 Best Fund Admin Software for VCs (2026 Compared). vcbeast.com

- Origin Investments. (2024). An Introduction to Private Real Estate Investment Fees. origininvestments.com

- Origin Investments. (2024). Comparing Private Equity Real Estate Fund Fees to Individual Deal Fees. origininvestments.com

- Anchin, Block & Anchin LLP. (2025). Key Considerations for Starting a Real Estate Fund, Part 2. anchin.com

- Callan Institute. (2025). Real Assets Fees: Exclusive 2024 Callan Study Digs Deep. callan.com

- Agora. (2025). Real estate fund administration: A complete guide. agorareal.com

- RCLCO Real Estate Consulting. (2024). Private Equi