President Donald Trump signed the One Big Beautiful Bill Act into law on July 4, 2025. Over the next several years, commercial real estate accounting and tax teams will need to respond to new compliance and regulatory requirements tied to this legislation.

At the same time, the industry is already feeling stretched. New regulations and compliance demands are driving hiring plans, with 38% of corporate tax departments planning to increase headcount. Hiring isn’t easy, though, and 83% of financial leaders report challenges finding qualified accounting talent. As firms look for ways to manage growing workloads with limited resources, interest in AI continues to rise.

To better understand how the industry is responding, Agora surveyed real estate accounting and tax professionals on current challenges and plans for the future.

Key findings

Key highlights from the survey results include:

-

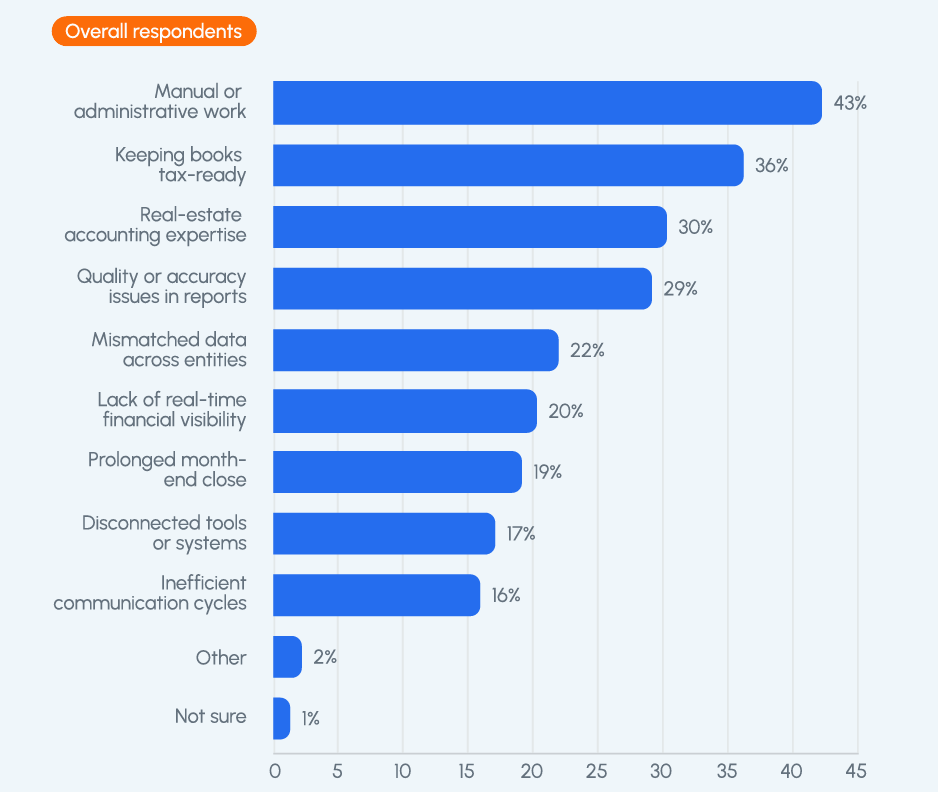

- 43% of firms cite manual or administrative work as their top challenge: Survey results also show operational and data-related issues, with 22% of respondents reporting mismatched data across reports and 20% stating they lack real-time visibility into financial performance. Firms in the Southwest report the highest impact from manual work, with 69% identifying it as their top issue.

- Monthly close takes 42% of firms five business days or less: The average monthly close time across respondents is 6.9 business days, and most firms report completing the close within five to ten business days.

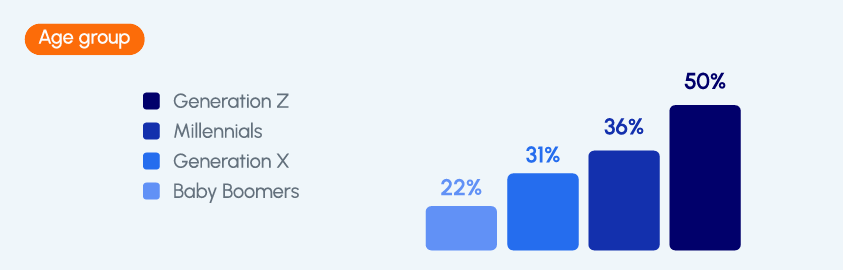

- 50% of Gen Z respondents report preparing for the One Big Beautiful Bill Act: Overall, 35% of firms say they are actively preparing for upcoming tax and compliance changes, while another 41% report monitoring developments. Preparation rates vary by age, with Gen Z showing the highest level of active preparation.

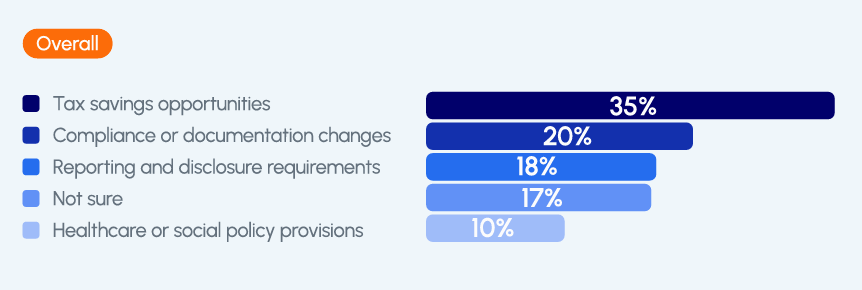

- For 35% of respondents, tax savings are the most anticipated outcome of OBBBA: Another 20% expect compliance and documentation changes to have the greatest impact, while 18% expect increased reporting and disclosure requirements.

- Respondents support AI adoption at 63%: Another 29% say they are very comfortable integrating AI into accounting and tax processes, while 34% report being somewhat comfortable. Respondents most often expect AI to improve report accuracy and error detection at 33% and automate data entry and reconciliations at 27%.

Research methodology

Agora worked with Talker Research to understand how real estate firms approach tax and accounting challenges and how they expect the One Big Beautiful Bill Act to affect their operations.

The survey gathered input from 200 senior professionals across the United States who oversee investment management or investor relations, including managing partners, CFOs, and investor relations managers.

Participants provided demographic information and answered questions on tax strategy, accounting processes, and expected regulatory changes. Talker Research conducted the study using a random double opt-in methodology, and its researchers are members of the Market Research Society and ESOMAR.

Manual work is a top accounting challenge

Manual work is a key accounting challenge for real estate firms, with 43% of respondents citing manual or administrative work as their top issue. Related challenges also add to this burden. Firms report issues with mismatched data at 22%, limited real-time visibility at 20%, and disconnected tools or systems at 17%.

Together, these factors help explain why firms estimate spending an average of 13.8 hours per month on manual data entry and reconciliation.

Most firms report relatively fast monthly closes

Survey results show that most firms close the books relatively quickly. In fact, 42% of respondents close the books in five business days or less, with an average close time of 6.9 business days.

Faster close cycles support timely performance reporting, especially as earlier research shows that 31% of investors expect detailed visibility into property performance and operations.

Preparation for tax and compliance changes varies across generations

Approaches to upcoming tax and compliance changes vary across firms. While 35% of respondents say they are actively preparing for changes related to OBBB, 41% say they are monitoring developments without taking action.

Readiness also varies by age group, with Gen Z reporting the highest level of active preparation at 50%.

What firms expect from the One Big Beautiful Bill

35% of respondents expect tax savings to be the main outcome of the OBBB.

In addition to potential tax savings, firms also expect changes to their day-to-day work. About 20% say compliance and documentation will have the biggest impact, while another 18% expect more reporting and disclosure requirements.

Respondents look to AI to reduce manual work

Most respondents are open to using AI in accounting and tax workflows. In the survey, 63% report being very or somewhat comfortable with AI adoption.

When asked where AI could make the biggest difference, 33% of respondents expect it to improve report accuracy and error detection, while 27% believe it can automate data entry and reconciliations. Others also expect AI to help speed up close processes and support audit readiness.

Wrapping it up

The survey shows that commercial real estate accounting is balancing efficiency with growing complexity. Most firms close the books quickly, but manual processes and data issues continue to create operational challenges.

As new regulations increase compliance requirements, accounting teams are being asked to do more with limited resources. Interest in AI continues to grow, with expectations around reducing errors and increasing automation.

How firms respond will impact their ability to deliver accurate information, support business decisions, and meet investor expectations.