In commercial real estate, the difference between a profitable deal and a costly mistake often comes down to one thing: the accuracy of your financial model. In my experience, a clear picture of your investment’s projected returns and risks helps you better evaluate deals and approach them with confidence.

What is commercial real estate financial modeling?

Real estate financial modeling is the process of forecasting a property’s financial performance over time. It relies on assumptions about the real estate market, the property in question, and the deal’s capital structure (equity vs. debt financing).

CRE professionals build real estate financial models with Microsoft Excel or other specialized software to evaluate the return potential of acquisition, value-add, and development projects.

Why commercial real estate financial modeling matters

Real estate financial modeling is an indispensable step in real estate investing. Here’s why:

Supporting investment decisions

By estimating a deal’s potential return, you can quickly determine whether it meets your return threshold. For example, if you’re targeting a minimum internal rate of return (IRR) of 8%, but the deal you’re looking at only offers a 7% IRR, you may want to pass on the opportunity.

In addition, real estate financial modeling can help you compare different deals. For example, let’s say you’re considering two different multifamily acquisitions. One has a projected IRR of 8%, and the other has a projected IRR of 9%. Then the latter may be the better deal.

Guiding deal structuring and capital planning

How you finance a deal can impact your final returns. This is why CRE professionals often distinguish between “unlevered” and “levered” returns. Unlevered returns describe the investment’s performance at the property level, while levered returns describe its performance once you factor in debt. By running financial models for both scenarios, you can optimize the deal’s capital structure for return potential. In some cases, more debt can lead to positive leverage, thereby boosting returns. In others, it can lead to negative leverage, lowering returns.

Managing financial risk through modeling

A dynamic financial model can also help you gauge investment risks. For example, you can use it to identify break-even points and potential downside scenarios with stress tests.

Start by adjusting key assumptions like vacancy rate and rent growth based on worst-case scenarios. From there, you can judge how much downside risk you’re willing to take on and/or create a contingency plan to mitigate it.

Types of commercial real estate financial models

There are different types of CRE financial models for different investment strategies:

1. Acquisition and underwriting models

Acquisition models are the most common and basic type of model. They are used to evaluate stabilized properties that already have tenants. As a result, the model focuses on the property’s purchase price, in-place cash flow, and financing options.

2. Value-add and repositioning models

Value-add models add a layer of complexity because they factor in renovation budgets, lease-up assumptions, and rent premiums. In other words, your returns not only depend on the purchase price, the eventual stabilized cash flow, and financing, but also on construction budgets and timelines, how fast you can attract new tenants, and by how much you can raise the rent.

3. Development and construction models

Real estate development models are similar to value-add models, except they involve even more complexity since you’re building from the ground up. Additional return factors include hard construction costs like site planning and excavation, and soft costs like permitting, design, and legal fees. Most projects also have loan draw schedules that impact cash flow projections.

4. Portfolio and fund-level models

Portfolio models aggregate performance projections across multiple properties. Meanwhile, fund-level models personalize return projections for general partners (GPs) and limited partners (LPs) based on their contributions and waterfall structures.

Components of a commercial real estate financial model

Here are the main components of a commercial real estate financial model:

| Component | Description |

| Key input assumptions and deal terms | These include purchase price, hold period, cap rate, loan terms, renovation costs, etc. |

| Revenue modeling: base rent, escalations, ancillary income | Revenue projections depend on current rent rolls, escalations outlined in leases, and any ancillary income from parking, storage, etc. |

| Operating expenses and vacancy forecasts | Operating expenses include management fees, maintenance, property taxes, insurance, etc. Vacancy and credit loss are based on historical performance and market averages. |

| Debt modeling and loan structure | CRE debt modeling and loan structures can vary widely. Think amortization schedules, interest-only periods, and refinancing assumptions. |

| Cash flow projections and exit planning | Cash flow can be calculated on a levered and unlevered basis. Meanwhile, exit sale proceeds depend on market and cap rate assumptions. |

| Return metrics like IRR and equity multiples | Internal rate of return (IRR), equity multiple (EMx), and other return metrics can be calculated on a levered and unlevered basis. |

Real estate financial modeling workflow step-by-step

Now that you know what goes into a CRE financial model, here’s how to build one from scratch:

Step 1: Collect property and lease data

Before you can build an accurate financial model, you need accurate data. Start by asking the seller or broker for the property’s historical operating expenses, rent roll, and lease abstracts. From there, you can also gather market comp data based on your own research.

Step 2: Define assumptions and timelines

Next, you must make assumptions about costs, revenue, and timelines. This means estimating the potential rent growth, operating expense inflation, lease-up pace, and construction duration. The more detailed your input assumptions, the better the model’s output will be.

Step 3: Build multi-year cash flows

This is where the fun begins. Use Excel or similar software to build a multi-year cash flow projection. For example, if you plan on a 10-year hold period, estimate the cash flow in each year based on expected revenues, expenses, capital expenditures (CapEx), and debt service.

Step 4: Run sensitivity and scenario tests

Once your model is built, you can run stress tests to see how the investment performs under best-case and worst-case scenarios. For example, adjust your assumptions for rent growth, cap rate, and expense inflation and observe the impact on the project’s returns.

Step 5: Create reports for stakeholders

Finally, you can create and tailor pro formas to share with other investors, lenders, and internal staff. That way, they can evaluate the deal based on its assumptions, key return metrics, and stress tests before committing.

Key metrics to track in CRE financial models

Before you build a CRE financial model, you must understand the key return outputs involved:

Net operating income (NOI)

Net operating income (NOI) measures how much income a property generates after accounting for operating expenses. It’s calculated by subtracting the latter from the former:

Internal rate of return (IRR)

Internal rate of return (IRR) measures an investment’s annualized return rate, while accounting for the size and timing of all cash flows during the holding period. It’s calculated by figuring out the discount rate at which the investment’s net present value (NPV) is zero. Since IRR can’t be solved algebraically in most cases, IRR is typically found using Excel’s (=IRR) function.

Equity multiple (EMx)

Equity multiple (EMx) is a ratio that measures how much total cash an investor receives for every dollar invested. It’s calculated by dividing total cash distributions by total equity invested:

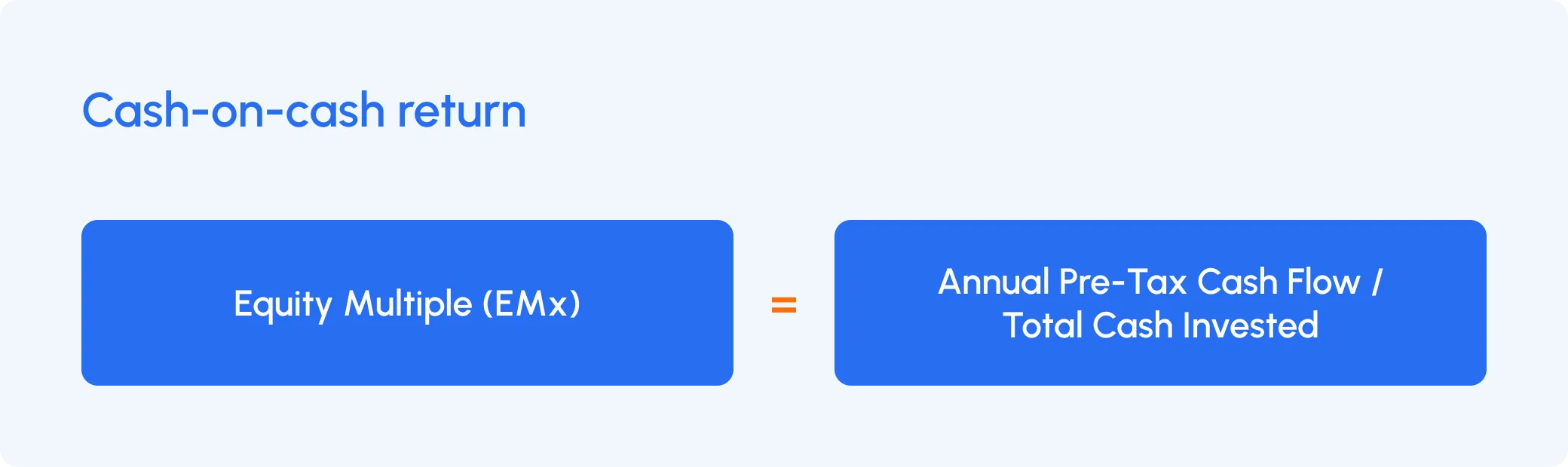

Cash-on-cash return

Cash-on-cash return measures your annual return as a percentage of how much cash you invested. It’s calculated by dividing annual pre-tax cash flow by total equity invested:

Debt-service coverage ratio (DSCR)

Debt-service coverage ratio (DSCR) measures a property’s ability to cover debt payments with its net operating income (NOI). It’s calculated by dividing annual NOI by annual debt service:

Common pitfalls in commercial real estate modeling

Avoid these common mistakes when modeling a commercial real estate deal:

| Common pitfalls | Description |

| Overly aggressive or faulty assumptions | Unrealistic estimates for rent growth, exit cap rate, or lease-up speed can inflate your expected returns, leading to disappointment. |

| Ignoring lease-up and vacancy periods | Novice CRE investors may forget to factor in lease-up and vacancy periods altogether, thereby skewing expected cash flows. |

| Oversimplified or incorrect debt modeling | Carefully review your financial model and have an experienced investor check it to avoid modeling mistakes and oversights. |

| Errors from manual data entry | Hard-coded (static) inputs, broken formulas, and inconsistent formatting from manual data entry can mess up your financial model. |

Best practices for building reliable models

To build a robust CRE financial model, follow these best practices:

- Use standardized modeling templates. As you model more and more deals, create model templates that you can reuse. This ensures consistency across deals and makes it easier to audit them.

- Keep market inputs current. The real estate market is constantly changing. To keep your model current, regularly update inputs like comps, loan terms, and interest rates.

- Run risk and scenario analyses. Stress testing helps you understand what you stand to lose on each deal, solidifying your confidence or lack thereof.

- Collaborate across teams. By gathering input from development, leasing, asset management, and other departments, you can make better investment decisions.

- Track versions and audit changes. Maintain a file version history of every financial model to make it easier to retrieve old data and to boost transparency during audits.

How financial modeling supports investor reporting and fundraising

Real estate financial modeling isn’t just about underwriting deals. It’s also an important step in fundraising and reporting on investment performance to investors.

Forecasting distribution timelines and returns

A complete financial model forecasts distribution timelines, along with expected returns. In other words, it’ll show when LPs and GPs can expect payments and how the investment will perform for them across IRR, EMx, cash-on-cash return, etc. This helps set expectations and build trust.

Communicating assumptions with clarity and consistency

Investors want to understand deal assumptions before committing their capital. A clearly labeled financial model can promote transparency by showing what inputs and formulas the projected returns rely on. A summary tab can also provide real-time updates on deal projections.

Visualizing exit strategies and upside potential for LPs

Add charts and graphs to your financial model to help investors visualize expected deal performance. For example, you could create visuals that show exit values, equity splits, and return waterfalls and highlight the upside potential for LPs.

Conclusion

Real estate financial modeling is more than just crunching numbers. It’s an essential skill that can help you derisk investments and gauge potential returns.

Whether you’re underwriting a stabilized asset or forecasting a multi-phase development project, a solid financial model can help align investor expectations, optimize deal structure for maximum return, and bring clarity to an otherwise opaque deal. CRE professionals who master financial modeling are better positioned to add value to their firm and advance in their careers.

As you practice real estate financial modeling, consider using Agora’s automated waterfall calculations that integrate seamlessly with the platform’s investor reporting features, making it easier than ever to promote transparency and foster trust.