Key takeaways

- Debt yield measures risk for commercial real estate lenders by showing how much NOI a property generates relative to the loan amount, offering insight into recovery potential if a borrower defaults.

- Independent of property value, debt yield uses only NOI and loan amount, making it immune to market price fluctuations and ideal for evaluating loan safety across varying capital structures.

- Higher debt yield signals lower lender risk, greater recovery likelihood in foreclosure, and is often preferred by CMBS lenders due to the nonrecourse nature of those loans.

- Borrowers can improve the debt yield by increasing a property’s net operating income (NOI) or by reducing the loan amount, for example, through a larger down payment. This enhances the property’s financial profile and reduces the lender’s perceived risk.

- Standard benchmark range for debt yield is 8–12%, with lenders favoring ratios at the higher end to minimize exposure and ensure sound underwriting decisions.

What is debt yield and its importance in commercial real estate

The debt yield ratio provides commercial real estate lenders with a measure of the risk they are taking when advancing funds to borrowers. It is one of the several metrics that lenders use and its primary benefit lies in helping to determine the return if the borrower defaults on the loan.

Commercial real estate lenders calculate the debt yield on a transaction by dividing the property’s net operating income (NOI) by the total loan amount. The ratio this calculation provides tells the lender how long it will take to get back the sum advanced if the borrower stops paying. Hence, from the lender’s viewpoint, a higher debt yield is a positive sign.

Remember that a higher debt yield ratio signifies a lower level of risk for the lender.

Why debt yield is considered an important ratio

The utility of this ratio lies chiefly in its ability to inform lenders of the risk inherent in a proposed loan. Here are several other reasons the commercial real estate financing industry turns to this ratio:

- Lenders use it to compare different loans. A loan that has a lower ratio carries more risk. Conversely, a loan with a higher ratio is a safer investment.

- The ratio tells lenders the cash flows they can expect if the borrower defaults.

- Lenders can calculate the number of years it would take to recoup their investment.

- The ratio is based on the loan amount. The market value of the property does not influence it. Consequently, it is not impacted by changing property prices.

- The ratio is calculated using the property’s NOI. As this figure does not consider financing costs, it is capital-structure neutral, making it especially useful in comparing different loans.

Did you know?

CMBS lenders heavily rely on debt yield because their loans are non-recourse. This means they depend solely on the asset’s cash flow for recoveries.

How to calculate debt yield

The calculation is straightforward. It involves dividing the property’s NOI by the total loan advanced. In other words, the ratio calculates how much money the property makes per year compared to the outstanding loan.

Debt yield formula

Net operating income: This figure represents the cash flow from a property after expenses. The first step in its computation involves adding the rental income to any other income the property generates. For example, the property could earn parking or vending machine fees in addition to rent.

The total revenue earned is reduced by the operating expenses incurred in connection with the property. These expenses include property taxes, sums spent on repairs and maintenance, property management fees, and utilities. The calculation does not consider capital expenses, income taxes, loan repayments (both principal and interest), and depreciation.

Loan amount: This figure represents the sum the commercial real estate lender plans to provide the borrower.

Debt yield calculation example

The following example will help clarify how the calculation works.

Consider a property that has a net operating income of $400,000. The loan advanced by the lender is $4,000,000. The ratio is calculated as follows:

Debt yield = $400,000 / $4,000,000 = 10%

At this point, it would be helpful to revisit what the ratio conveys. If the borrower defaults and the lender has to take over the property, the ratio helps calculate the number of years it would take to recover the original investment. In the above example, the lender would recover 10% yearly, taking ten years to recover the complete investment.

Bear in mind that the computation uses the NOI, and this figure does not consider financing costs or income taxes. Hence, the ratio is best used to compare different loans.

Debt yield compared to other commercial mortgage risk metrics

Many lenders value this ratio for one simple reason. It remains unaffected by external market-related factors like variations in interest rates and rapidly increasing property prices. It is an excellent risk metric if prices signal a real estate bubble.

However, at this stage, examining a few other metrics that commercial lenders commonly use to evaluate loan proposals can also be pertinent.

Loan to value (LTV) vs debt yield

The loan to value ratio computation involves dividing the loan advanced by the property value. In other words, the LTV tells you the percentage of the loan amount to the property’s appraised value. A crucial feature of this ratio is that it is based on the property’s value, a factor that can contribute to rapid changes in the ratio.

- LTV calculator

LTV ratios of between 65% and 80% are the norm. However, the ratio is also influenced by the property type and class as well as the debt service coverage ratio for the property in question.

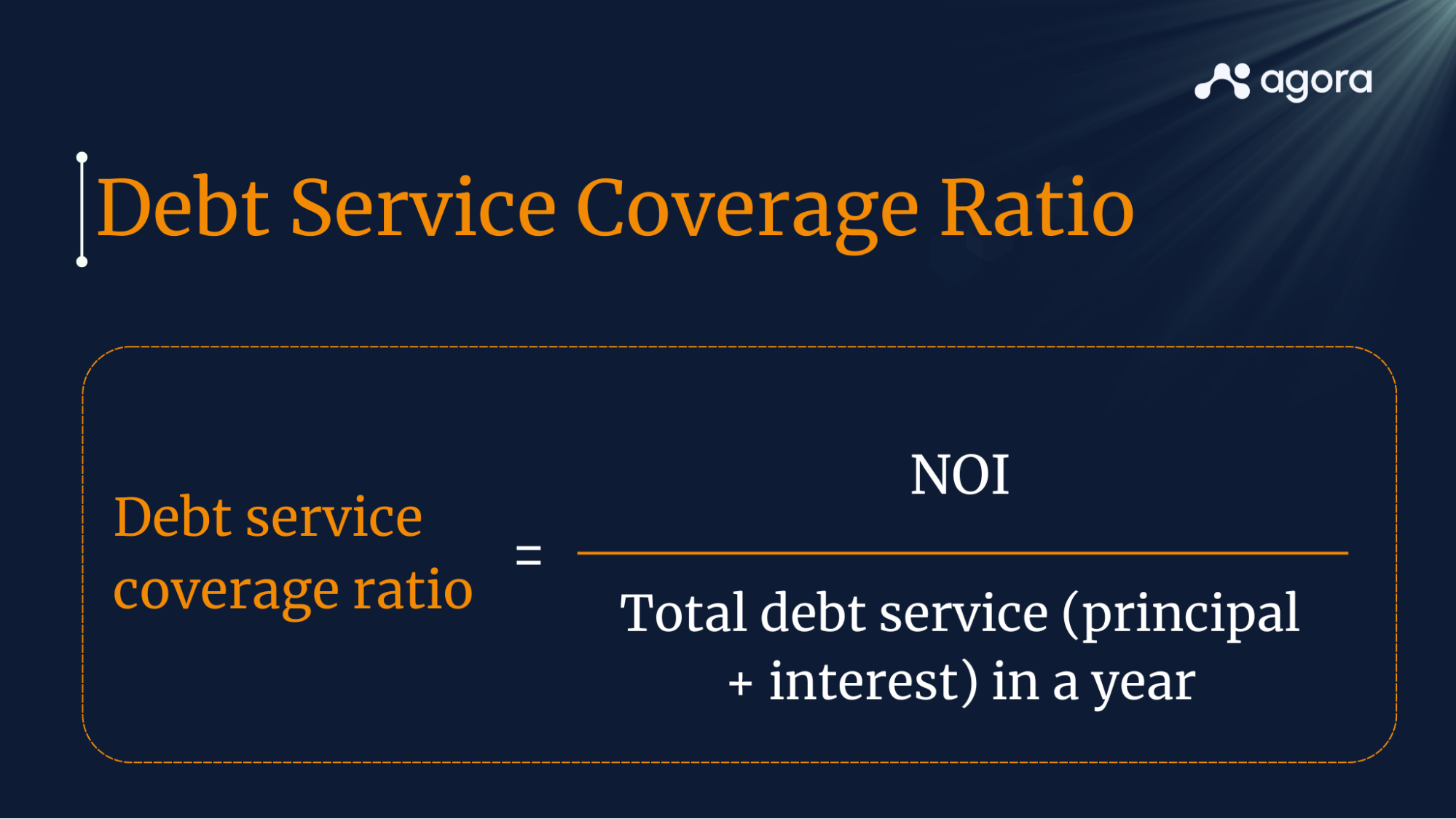

Debt service coverage ratio (DSCR) vs debt yield

The DSCR quantifies the borrower’s ability to pay off the loan. It is the ratio of the NOI to the debt obligations (both principal and interest) for a specific period. A higher DSCR indicates a greater ability to service the loan.

- DSCR calculator

Cap rates vs debt yield

The capitalization rate or cap rate is another favorite in the CRE industry. It is computed by dividing the property’s NOI by its current value. As property prices can fluctuate with market conditions, this ratio can be prone to rapid changes.

- Cap rate calculator

The following table summarizes how debt yield differs from the three other CRE risk metrics described in this section of the post:

| Risk metric | Formula | How it is helpful |

| Debt yield | NOI/Loan amount | Tells lenders the cash inflows they can expect if the borrower defaults |

| LTV | Loan amount/Appraised property value | Percentage of the loan amount to the property’s appraised value |

| DSCR | NOI/Debt service (principal + interest) | Tells lenders about the ability of the borrower to meet their debt service obligations |

| Cap rate | NOI/Market value of property | A ratio that compares the income from the property to its value |

Pros and cons of debt yield in commercial real estate

The foremost advantage of this ratio is that it tells lenders how much they can expect to recover from the property if it goes into foreclosure. Therefore, a high ratio can be a significant advantage from the lender’s perspective. On the other hand, a low ratio should be viewed as a red flag.

Benefits of a high debt yield

- In a property foreclosure, lenders stand a better chance of recovering their dues.

- There is a lower likelihood of default.

- A higher ratio represents a lower level of risk for the lender.

Risks of a low debt yield

- Implies a high-risk proposition for the lender.

- If the ratio is low, the lender should see if they can obtain any other form of security, such as a personal guarantee from the borrower.

- In the event of default, the lender’s recoveries will be lower. It would take more time to recoup dues.

Strategies to increase debt yield in commercial real estate

Here are two ways borrowers can effectively increase the debt yield in a transaction. If they are successful, it can help them get their loan application approved:

- Increasing the net operating income of the property: A higher NOI results in a higher debt yield. This works in the borrower’s favor as it implies a lower level of risk for the lender.

- Increasing the term of the loan: A longer loan term gives the borrower more time to repay, leading to a lower outgo towards interest and principal repayments. This gives the lender a greater assurance that repayment commitments will be honored.

What is a good debt yield?

Lenders prefer a higher ratio – the higher, the better. However, a good benchmark is a ratio between a minimum debt yield of 8% and a high of 12%. Remember that a higher ratio signifies a lower risk of default and vice versa.

Which lenders look at debt yields?

Debt yields provide lenders with an uncomplicated way to assess a property’s income-generating capacity. As a result, many commercial real estate financing professionals use this metric.

CMBS (commercial mortgage-backed securities) lenders are especially partial to this ratio. The reason? CMBS loans are nonrecourse. Lenders cannot attach the borrower’s personal property in the event of default. Hence, they can only rely on the income-generating capacity of the financed property to recover their dues.

The bottom line

Debt yield is an excellent metric for commercial real estate lenders, especially those who provide nonrecourse loans. It tells lenders how quickly they can recover their money if the borrower defaults. The ratio is popular with lenders as it remains unaffected by changes in property prices and simultaneously measures the property’s ability to service debt.